Senior Debt Investing Explained: First Lien, Collateral, Covenants and How to Protect Your Capital

In today’s investment environment, where volatility and uncertainty continue to shape decision-making, capital preservation has become just as important as capital growth. Investors are increasingly looking for structures that offer predictability, downside protection and clear priority in repayment. This is where senior debt stands out.

Senior debt sits at the top of the capital stack and plays a foundational role in real estate and commercial investments. It is often considered one of the most secure ways to participate in deals, especially for those who prioritize consistent income and risk mitigation over aggressive upside.

Understanding how senior debt works, what “first lien” really means and how collateral and covenants protect investors can help you make more informed investment decisions. Whether you are new to real estate investing or looking to diversify your portfolio, this guide breaks down everything you need to know in a simple, practical way.

What Is Senior Debt

Senior debt is the primary loan secured against a property or asset. It is called “senior” because it has the highest priority in the capital stack meaning it gets repaid first before any other investors receive returns.

In a typical deal structure, senior debt is provided by banks, credit funds or private lenders. These lenders are not equity partners. They do not participate in profits beyond the agreed interest payments. Instead, they focus on steady income and capital protection.

Key Characteristics of Senior Debt

- First priority in repayment

- Secured by the underlying asset

- Fixed or floating interest payments

- Lower risk compared to equity investments

- Limited upside potential

Because of these characteristics, senior debt is often seen as a conservative investment option especially during uncertain market cycles.

Understanding the Capital Stack

To fully grasp the value of senior debt, you need to understand where it sits in the capital stack. The capital stack represents the hierarchy of financing in a deal and defines who gets paid, in what order and how risk is distributed among investors.

From top to bottom, it typically looks like this:

- Senior Debt

- Mezzanine Debt

- Preferred Equity

- Common Equity

Each layer comes with a different level of risk and return and this structure is what ultimately determines how secure or speculative an investment may be. Senior debt sits at the top, meaning it holds the strongest position in terms of repayment priority. Because of this, it is generally considered the safest layer in the stack. On the other hand, common equity sits at the bottom, absorbing the most risk but also offering the highest potential upside if the project performs well.

As you move down the capital stack, risk increases because each layer depends on the performance of the layers above it. For example, mezzanine debt and preferred equity investors only get paid after the senior debt obligations are fully satisfied. Common equity investors are last in line, meaning they only see returns after all other stakeholders have been paid.

This hierarchy becomes especially important in downside scenarios. If a project underperforms, faces financial distress or is forced into a sale, the available proceeds are distributed according to this structure. Senior debt holders are paid first from any available funds, followed by mezzanine lenders then preferred equity investors and finally common equity holders if anything remains.

This priority of payment is what makes senior debt particularly attractive to risk-conscious investors. It provides a layer of protection that is not available in lower positions of the stack, helping preserve capital even when a deal does not go as planned.

What Does “First Lien” Actually Mean

The term “first lien” is one of the most important concepts in senior debt investing.

A lien is a legal claim against an asset. When a lender has a first lien, it means they have the primary legal right to seize and sell the asset if the borrower defaults on the loan.

Why First Lien Matters

- It gives lenders control over the asset in a default scenario

- It ensures priority repayment before any other claims

- It significantly reduces the risk of capital loss

In simple terms, being in a first lien position means you are first in line. If something goes wrong, your investment is protected by the value of the underlying asset.

For example, if a property is sold due to foreclosure, the proceeds go first to the senior lender with the first lien. Only after that are other lenders or equity investors paid, if any funds remain.

The Role of Collateral in Senior Debt

Collateral is another key component that strengthens the security of senior debt investments.

Collateral refers to the asset that backs the loan. In real estate, this is typically the property itself. In other types of investments, it could include equipment, receivables or other valuable assets.

How Collateral Protects Investors

- Provides a tangible asset backing the loan

- Can be liquidated to recover funds in case of default

- Helps maintain discipline in underwriting and lending

The quality and value of the collateral are critical. Lenders usually perform detailed due diligence to ensure that the asset is worth more than the loan amount. This creates a buffer known as the loan to value ratio.

Loan to Value and Risk

Loan to value or LTV measures how much of the asset’s value is financed by the loan. For example, a 65 percent LTV means the loan covers 65 percent of the property’s value.

Lower LTV ratios provide greater protection because there is more equity beneath the debt. This cushion reduces the likelihood of loss even if property values decline.

Covenants: The Rules That Protect Lenders

Covenants are conditions written into the loan agreement that the borrower must follow. They act as safeguards to ensure that the borrower manages the asset responsibly and maintains financial stability.

There are two main types of covenants: financial and operational.

Financial Covenants

These relate to the financial performance of the borrower or the property.

Examples include:

- Maintaining a minimum debt service coverage ratio

- Limiting additional borrowing

- Ensuring sufficient cash flow to cover payments

Operational Covenants

These focus on how the asset is managed.

Examples include:

- Keeping the property insured

- Maintaining the asset in good condition

- Providing regular financial reporting

Why Covenants Matter

Covenants give lenders early warning signs if something starts to go wrong. If a borrower violates a covenant, the lender can step in before the situation worsens.

This proactive protection is a major advantage of senior debt compared to equity investments, where investors often have less control.

Income Stability and Predictability

One of the biggest benefits of senior debt is the predictability of returns. This consistency makes it a reliable option for investors who prioritize steady cash flow over market-driven gains.

Unlike equity investors who rely on property appreciation and profit sharing, senior debt investors receive regular interest payments. These payments are typically structured as:

- Monthly or quarterly distributions

- Fixed or floating interest rates

- Contractual obligations regardless of performance

Because these terms are predefined, investors have clear visibility into their expected income throughout the investment period. This makes financial planning and cash flow management much easier.

This makes senior debt especially appealing for investors seeking steady income rather than speculative gains while also helping reduce overall portfolio volatility.

Risk Profile of Senior Debt

While senior debt is considered lower risk, it is not risk free. Understanding the potential risks helps investors make better decisions.

Key Risks to Consider

Default Risk

If the borrower cannot make payments, the lender may need to foreclose on the asset.

Market Risk

Declines in property value can reduce the effectiveness of collateral protection.

Interest Rate Risk

Changes in interest rates can impact returns especially for floating rate loans.

Liquidity Risk

Senior debt investments may not always be easy to exit before maturity.

Despite these risks, the combination of first lien position, collateral backing and covenants makes senior debt one of the more secure options available.

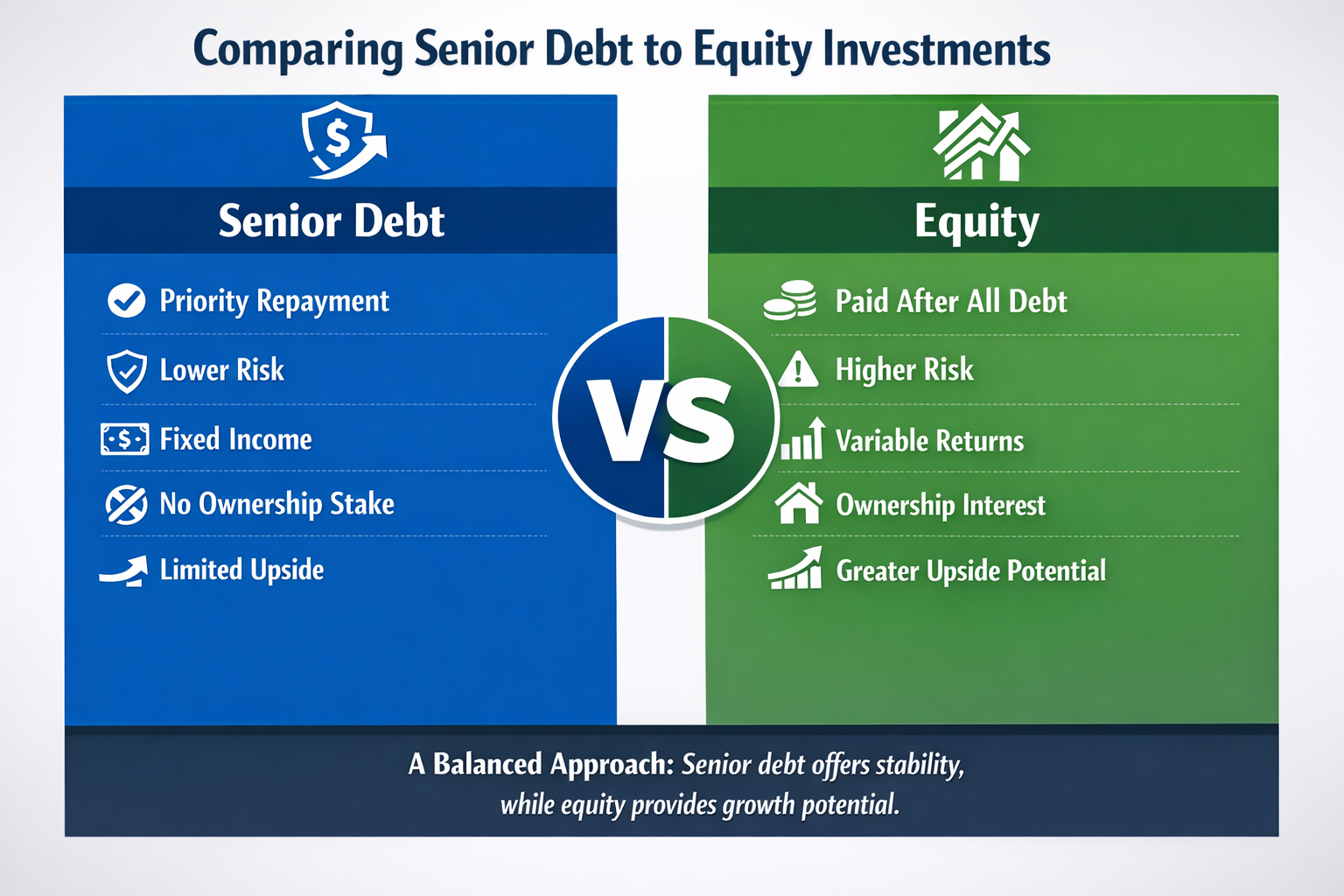

Comparing Senior Debt to Equity Investments

Senior debt offers priority repayment, lower risk and predictable fixed income, making it a more stable investment option. In contrast, equity comes with higher risk but provides ownership and greater upside potential. Understanding this balance helps investors use senior debt to stabilize their portfolios while still pursuing growth through equity.

When Senior Debt Makes the Most Sense and How to Evaluate It

Senior debt is not always the best choice for every investor or every deal but it becomes especially valuable in certain situations where stability and protection are priorities. It tends to perform best for investors seeking consistent income, those following conservative investment strategies or during uncertain and volatile market conditions. It is also a strong fit for portfolio diversification and for investors focused on preserving capital while still generating reliable returns.

Because of its lower risk profile and priority position, senior debt can act as a stabilizing force within a portfolio. It helps balance higher risk investments such as equity by providing predictable income and reducing overall volatility, ultimately contributing to a more resilient investment strategy.

Before committing capital, however, it is important to evaluate each senior debt opportunity carefully. Not all deals are structured the same and the strength of the investment depends heavily on its underlying fundamentals.

Some key questions to ask include:

- What is the loan to value ratio?

- What type of collateral secures the loan?

- Are there strong covenants in place?

- What is the borrower’s track record?

- How stable is the underlying asset?

- What is the exit strategy for repayment?

Taking the time to assess these factors can help you identify well-structured deals, minimize risk and ensure that the investment aligns with your financial goals.

The Strategic Role of Senior Debt in a Portfolio

Senior debt can play a powerful role in building a balanced investment strategy.

It provides:

- Income stability

- Downside protection

- Reduced volatility

- Diversification across asset classes

By combining senior debt with other investment types such as preferred equity and common equity, investors can create a layered approach that aligns with their risk tolerance and financial goals.

Final Thoughts

Senior debt offers a compelling combination of security, structure and predictability. Its first lien position ensures priority repayment, collateral provides tangible protection and covenants enforce discipline throughout the life of the investment.

For investors who value consistency and risk management, senior debt can serve as a strong foundation within a diversified portfolio. While it may not deliver the highest returns, it often delivers something just as important: reliability.

At Prawdzik Capitals, structuring investments with clarity, protection and long term performance in mind is a core focus. Understanding how senior debt works is not just about learning terminology. It is about recognizing how capital can be positioned intelligently to navigate both opportunity and risk.

When used strategically, senior debt is not just a safer option. It is a smarter one.